AccessMobility News & Assets Community for

mobilitynews clippings, thought-leadership articles,

on-demand podcasts, webcasts and other assets of essential

intelligence- contributed by our team of experts and

partners.]

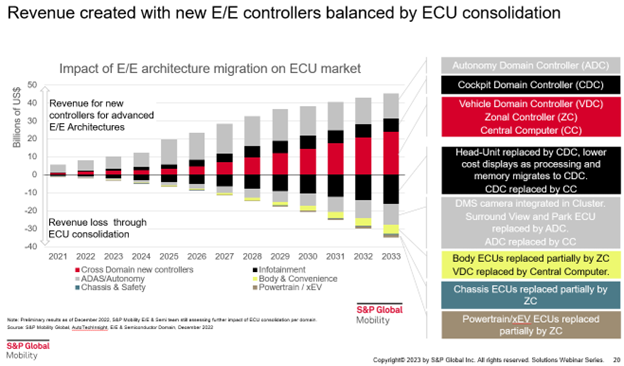

Evolving E/E architecture will drive the adoption of new

hardware based on domain and zone controllers, and eventually,

central computers. According to recent research by S&P Global,

addressable markets for control units will amount to an estimated

$40 billion of new ECU business in 2033 for Tier 1s—mostly for

autonomy-, cockpit-, and vehicle-domain controllers. Below the

line, the total market is offset by the consolidation of existing

ECUs as their functions are eventually absorbed into these more

powerful units. The result is still a net market plus, but the

replacement of existing ECUs will hit some suppliers harder than

others.

What’s at stake? S&P Global research shows that the

electronic ECUs in the various domains in the vehicles will start

to coagulate into fewer, larger hardware boxes with powerful

computers inside that address hardware in several or even all

domains. The cross-domain nature of these devices will challenge

suppliers—a zone controller integrates ECUs from various

domains based on location. Companies with narrow product offerings

such as cockpit or body ECUs that do not make ADAS ECUs will need

to partner with other tier 1s. This leads to revenue sharing and is

less attractive to OEMs seeking single solutions.

These “domain controllers” will thus cross domains in the

future, and the ability to serve several domains depends on the

knowledge base of the supplier. An example might be a powerful

Vehicle Domain Controller with a combined body, powertrain, and

chassis functions, or a central computer, e.g., with combined ADAS

and infotainment domains. These integration roadmaps will mean

specialized Tier 1s with single domain coverage must cooperate to

remain relevant—such as Magna (pure ADAS) and LG Electronics

(pure Infotainment) while others Bosch, Continental, Denso, or

Aptiv benefit from wider tool kits.

Find out more through the EE Architecture Revolution Webcast: https://lnkd.in/gfwE6cGu

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://www.spglobal.com/mobility/en/research-analysis/swings-and-roundabouts-who-benefits-from-new-ee-architecture.html

- :is

- ][p

- a

- ability

- According

- ADAs

- address

- Adoption

- All

- amount

- and

- aptiv

- architecture

- ARE

- article

- articles

- AS

- Assets

- At

- attractive

- base

- based

- BE

- below

- benefit

- benefits

- Billion

- body

- Bosch

- boxes

- business

- by

- central

- challenge

- chassis

- Cockpit

- combined

- community

- Companies

- computer

- computers

- consolidation

- continental

- contributed

- control

- controller

- COOPERATE

- coverage

- Cross

- data

- depends

- Devices

- Division

- domain

- domains

- drive

- e

- Electronic

- Electronics

- essential

- estimated

- Ether (ETH)

- Even

- eventually

- example

- existing

- experts

- For

- from

- functions

- future

- Global

- Hardware

- Hit

- HTML

- HTTPS

- in

- Integrates

- integration

- knowledge

- larger

- Leads

- LG

- LG Electronics

- Line

- location

- make

- managed

- Market

- Markets

- might

- mobility

- more

- Nature

- Need

- net

- New

- news

- of

- Offerings

- offset

- on

- On-Demand

- Other

- Others

- partner

- partners

- plato

- Plato Data Intelligence

- PlatoData

- plus

- Podcasts

- powerful

- Product

- published

- ratings

- recent

- remain

- research

- result

- revenue

- Revolution

- roadmaps

- s

- S&P

- S&P Global

- seeking

- serve

- several

- sharing

- Shows

- single

- Solutions

- some

- specialized

- stake

- start

- Still

- such

- suppliers

- Swings

- team

- that

- The

- their

- These

- Through

- tier

- to

- tool

- Total

- units

- various

- vehicle

- Vehicles

- which

- while

- WHO

- wider

- will

- with

- zephyrnet