Wall Street expected a beat, but today’s “blistering” CPI was an overheating “shock” and the Fed is about to start sweating.

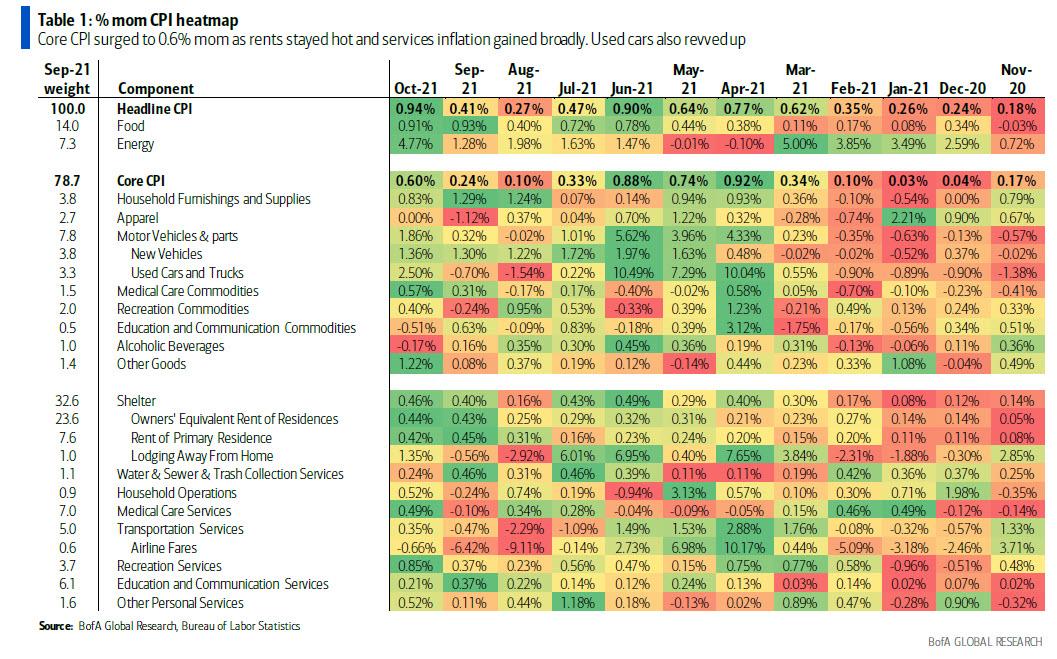

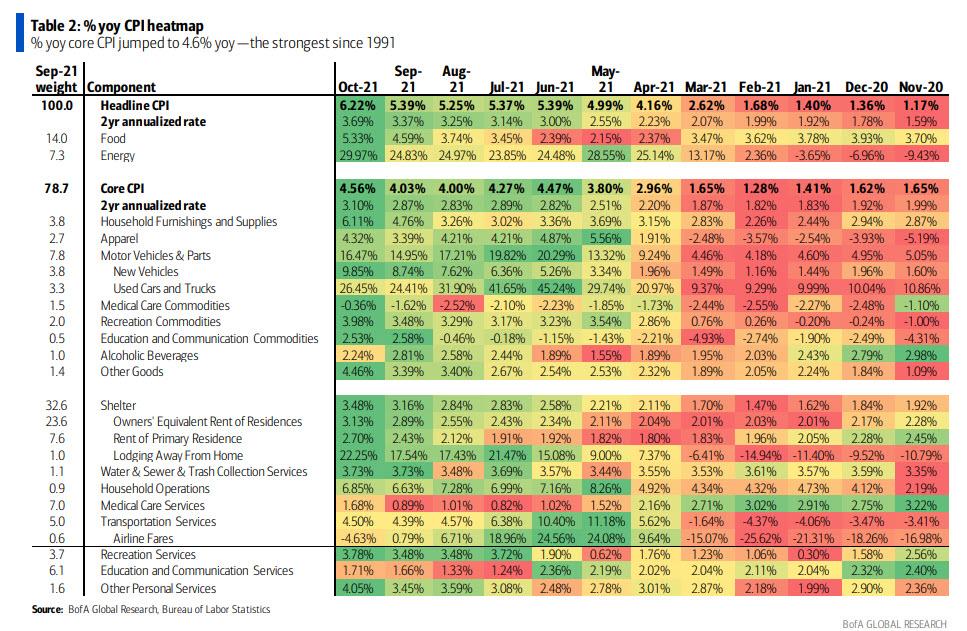

As we detailed earlier, core CPI surged to a 0.6% in October, boosting the % yoy rate to 4.6% from 4.0% – the highest since 1991. Headline CPI spiked 0.9% (0.94% unrounded), nearly rounding to a 1.0% print. This caused the % yoy rate to soar to 6.2% (6.22% unrounded) from 5.4%, which was the highest since 1990. Headline received further boosts from energy (+4.8%) and food (+0.9% mom for second month). The details within the report signaled strengthening persistent pressures though transitory forces also picked up. The data point to a strong October core PCE reading of 0.4% mom and 4.0% yoy.

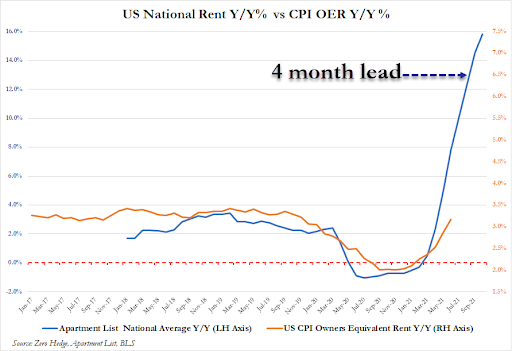

As we have been warning for much of the past 3 months, Owners’ equivalent rent and rent inflation were a big focus for this month: they printed a 0.4%+ mom clip for a second time providing additional confirmation of a reset to a higher trend. Rents are the biggest cyclical driver of inflation and therefore the most crucial component to monitor for persistent price pressures. And, as we have noted repeatedly this year, in recent months they are only going higher based on real time rental indicators.

Another “sticky” inflation component – medical care services – surged 0.5% mom as healthcare insurance soared 2.0% mom, a trend which Bank of America economists expect to continue through next August—while hospital services rose 0.5% mom.

Adding to the stronger persistent inflation story, we saw broad-based gains across major services categories, which could reflect positive feedback between prices and strong wages.

As BofA’s Alexander Lim writes, “the heat seen in rents and across services could make the Fed begin to sweat as they wait out the return in the labor supply and easing of supply constraints over the coming months.” Clearly, Lin adds, “the risks are for the timing of rate hikes to be pulled forward”, so stay tuned to shifts in Fed communication.

Meanwhile, it wasn’t just persistent inflation that soared: pandemic and reopening-related pressures also returned in force this month: used cars surged 2.5% mom and new cars stayed hot at 1.4% mom. Lodging rose 1.4% mom while airline fares fell 0.7% mom, though the latter was impacted by significantly unfavorable seasonal factors. Outside of autos, core goods were mixed as household furnishings & supplies, recreation, and other goods were up, but apparel was flat and education & communication and alcohol fell (spoiler alert: this is a lie). This could reflect the earlier start to the holiday shopping season for some retailers, which would mean a positive payback next month.

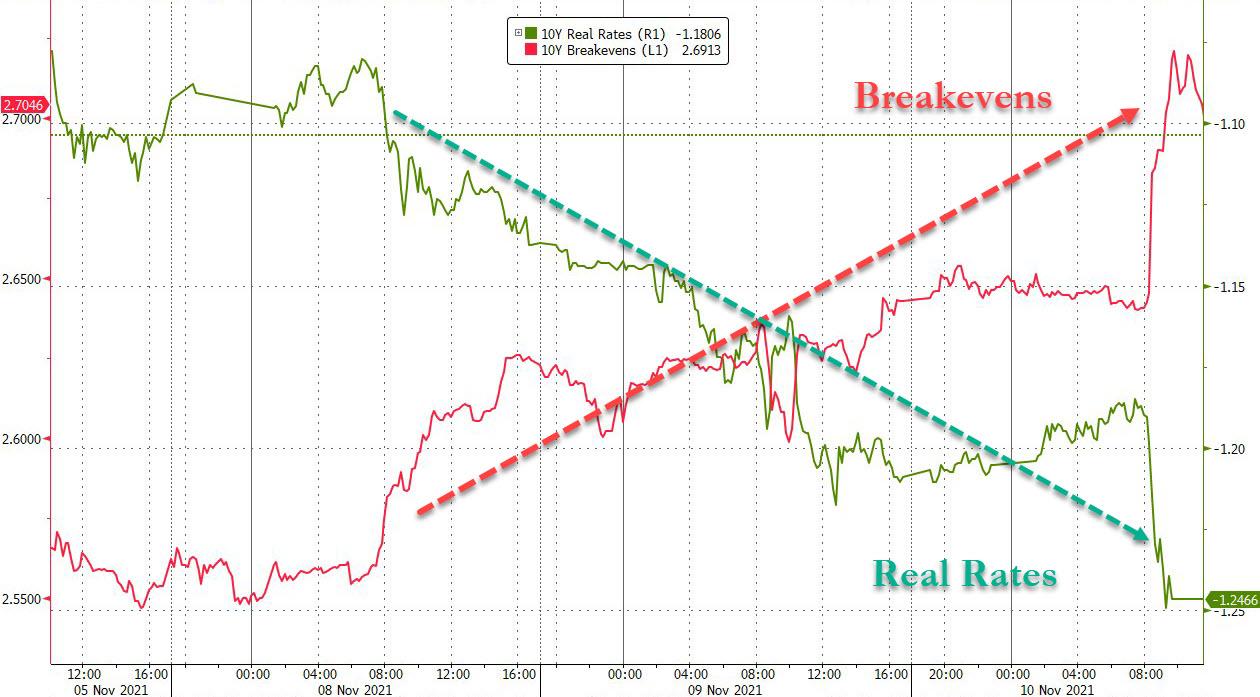

Commenting on the market reaction, BofA writes that given the strength in persistent components, the bear flattening of the curve is consistent with what we expected. Nominal rates increased 5- 7 bps in the front end-and belly while longer tenor rates were little changed. Inflation breakevens drove the move higher in nominal rates, while reals collapsed across the curve as bonds are screaming stagflation and/or eventual recession

The Eurodollar curve steepened out to late ’22 to mid ’24 expiries, with the market pricing an additional 13 bps of hikes by mid-’23. Further out the curve, however rates were little changed: 5y5y inflation breakeven declined 3 bps and 5y5y OIS was flat. The market response reflects the pulling forward of rate hikes alongside elevated near-term inflation, while longer term inflation expectations are little changed.

Finally, here is a heatmap of MoM CPI…

… And here is YoY CPI.

- &

- 7

- Additional

- airline

- Alcohol

- america

- apparel

- Bank

- Bank of America

- Biggest

- Bonds

- boosting

- care

- cars

- caused

- coming

- Communication

- component

- continue

- curve

- data

- driver

- easing

- Education

- energy

- Fed

- Focus

- food

- Forward

- goods

- healthcare

- here

- Hospital

- household

- HTTPS

- image

- inflation

- insurance

- IT

- labor

- major

- Market

- medical

- medical care

- mixed

- mom

- months

- move

- Other

- owners

- pandemic

- price

- pricing

- pulling

- Rates

- reaction

- Reading

- Rent

- report

- response

- retailers

- Services

- Shopping

- start

- stay

- street

- supply

- time

- wait

- within