Reg CF is off and running, on its way to becoming the way most American companies raise capital. Still, there are three things that would improve the Reg CF market significantly.

Revise Financial Statement Requirements

Financial disclosures are at the heart of American securities laws, I understand. The best way to understand an established company is often to pore over its audited financial statements, footnotes and all.

But that’s just not true of most small companies, whether the micro-brewery on the corner or a new social media platform. For these companies, reviewed or audited statements yield almost no worthwhile information to prospective investors. Yet the cost of the statements and the time needed to create them are significant impediments in Reg CF.

In my opinion, the following financial disclosures would be more than adequate:

- Copies of the issuer’s tax returns for the last two years;

- Interim financial statements (profit and loss and balance sheet) from Quickbooks or other financial software, through the last day of the month before the offering is launched;

- A separate statement of the issuers’ assets and liabilities in Form C;

- An attestation from the Chief Executive Officer;

- A statement in Form C describing where and how the issuer expects to derive revenue during the next 12 months (e.g., subscription fees, advertisements, rents, etc.);

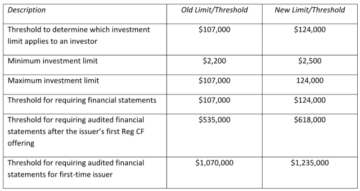

- Reviewed financial statements for offerings in excess of $1,235,000; and

- No requirement for audited statements.

Conversely, I believe annual audited financial statements should be required after a successful raise.

Address Artificially Low Target Amounts

Artificially low target amounts are the worst thing about Reg CF, by a long shot.

In the common approach, a company that needs $750,000 to execute its business plan sets a target amount of $25,000.

The artificially low target works for both the platform and the company. If the company raises, say $38,000, then the platform receives a small commission and advertises a “successful” offering, while the company can at least defray its costs.

But investors have thrown their money away.

Artificially low target amounts are terrible for investors and terrible for the industry, in a vicious cycle. Nobody wants to throw money away, and with so many Reg CF offerings using artificially low target amounts many serious investors will simply stay away from the industry.

Speaking of the Vietnam war, John Kerry asked “Who wants to be the last man to die for a lie?” Here, the question is “Who wants to be the first to invest in a company that needs a lot more?”

The fix is pretty simple. Issuers should be required to disclose what significant business goal can be accomplished if the offering yields only the minimum offering amount or, if no significant business goal can be achieved, should be required to say so.

In the meantime, it’s pretty shocking that while many offerings use an artificially low target amount, very few disclose the enormous additional risk to early investors. That’s a lot of lawsuits waiting to happen.

More Automation for Issuers

Speaking of lawsuits waiting to happen. . .

Most platforms do a pretty good job automating the process with investors. With issuers not so much.

Instead, platforms interact with issuers through people. Theoretically the role of these people is simply to guide the issuer through a semi-automated process. In practice, however, they end up as all-purpose advisors, giving issuers advice about everything from the type of security the issuer should offer to the issuer’s corporate structure to whether an SPV should be used.

As nice and well-meaning as these people may be, they aren’t qualified to give all that advice. Too often they end up giving advice that is either incomplete or wrong, doing a disservice to issuers and creating an enormous potential liability for the platform.

It’s unrealistic to think the platform will staff a team of investment bankers and securities lawyers giving individual advice to each issuer. Instead, in my opinion, the solution is to do a much better job automating the issuer side of the platform. That’s easier said than done, I realize. I hope and expect that the software providers active in Reg CF can provide some industry-wide solutions.

Questions? Let me know.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: https://crowdfundingattorney.com/2022/10/06/three-ways-to-improve-reg-cf/

- 000

- 12 months

- a

- About

- accomplished

- achieved

- active

- Additional

- advice

- advisors

- After

- All

- American

- amount

- amounts

- and

- annual

- approach

- Assets

- audited

- automating

- Automation

- Balance

- Balance Sheet

- bankers

- becoming

- before

- believe

- BEST

- Better

- business

- capital

- chief

- chief executive officer

- commission

- Common

- Companies

- company

- Corner

- Corporate

- Cost

- Costs

- create

- Creating

- day

- Die

- Disclose

- doing

- each

- Early

- easier

- either

- enormous

- established

- etc

- everything

- execute

- executive

- Executive Officer

- expect

- expects

- Fees

- few

- financial

- First

- Fix

- following

- For Investors

- form

- from

- Give

- Giving

- goal

- good

- good job

- guide

- happen

- Heart

- here

- hope

- How

- However

- HTTPS

- improve

- in

- individual

- industry

- information

- instead

- interact

- Invest

- investment

- Investors

- Issuer

- Job

- John

- Know

- Last

- launched

- Laws

- Lawsuits

- Lawyers

- liabilities

- liability

- Long

- loss

- Lot

- Low

- man

- many

- Market

- meantime

- Media

- minimum

- money

- Month

- months

- more

- most

- needs

- New

- next

- offer

- offering

- Offerings

- Officer

- Opinion

- People

- plan

- platform

- Platforms

- plato

- Plato Data Intelligence

- PlatoData

- potential

- practice

- pretty

- process

- Profit

- provide

- providers

- qualified

- question

- Quickbooks

- raise

- raises

- realize

- receives

- Reg

- required

- requirement

- returns

- revenue

- reviewed

- Risk

- Role

- running

- Said

- Securities

- Securities Laws

- security

- serious

- Sets

- should

- significant

- significantly

- Simple

- simply

- small

- So

- Social

- social media

- Software

- solution

- Solutions

- some

- SPV

- Staff

- Statement

- statements

- stay

- Still

- structure

- subscription

- successful

- Target

- tax

- team

- The

- their

- thing

- things

- three

- Through

- time

- to

- too

- true

- understand

- use

- Vietnam

- Waiting

- war

- ways

- What

- whether

- while

- will

- works

- Worst

- worthwhile

- would

- Wrong

- years

- Yield

- yields

- zephyrnet